|

|

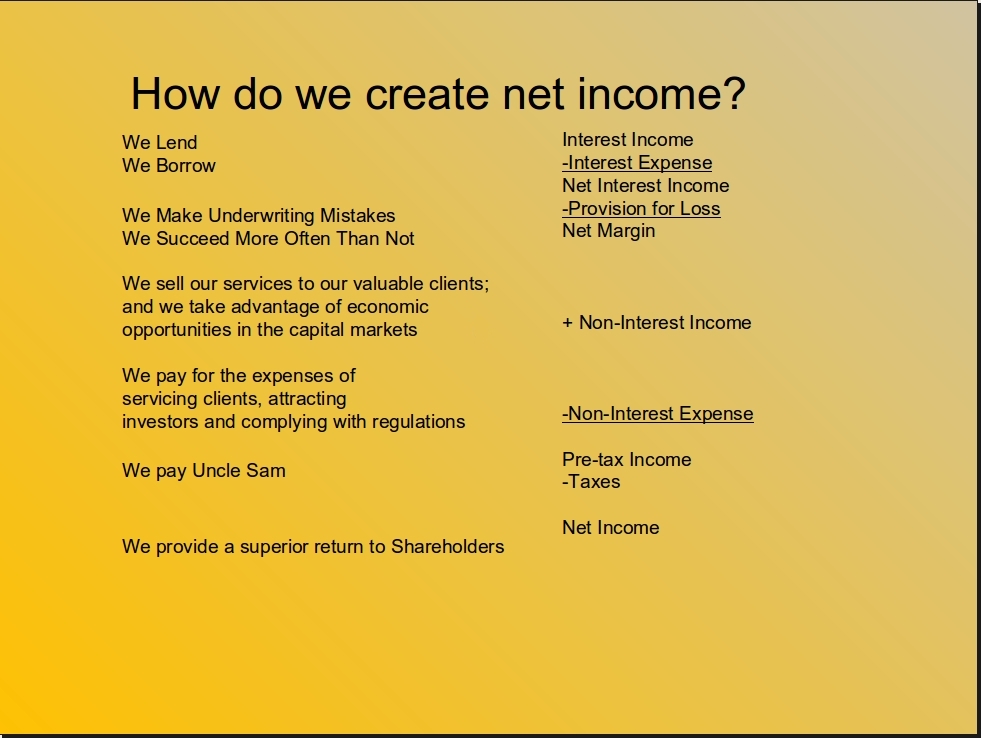

Teaching Our Employees How We Make Money

Here's what your employees will appreciate understanding: The bank rents money to customers (loans) and gets a rental fee from it. It also serves as a parking spot for clients' money (deposits), and it pays a parking fee for the use of the money. Interest-free checking accounts have no fee associated with them, which is what makes them most profitable for the bank. The difference between the two numbers is our margin. This part accounts for about 80% of most community bank's income. We also charge fees for the services we provide, and those account for 20% of our income. The greater this amount, the less capital we need to have in order to operate the bank. The rest is self explanatory. I further believe that employees can readily understand that all bank capital, whether you're private or public, is allocated heartlessly, based upon returns. Further, capital markets raise their expectations for returns every year, which explains why banks must expect greater results from their own employees every day. It's not executive management's whim that bring them to ask for more each year; it's their own boss, the board, as a representative of the shareholder(s), which is the reason why the bar gets raised annually, to ensure that the bank continues to hold on to its capital and make an attractive investment for others. If you want your employees to consider shareholders in their decision-making, you need to give them the tools to do so. This doesn't necessarily mean pricing models, although those can be excellent reminders of the importance of products such as core deposits and Treasury management to the overall profitability of the bank. It does entail a commitment to educate your employees on how banks make money, including entry-level people in both the front and back offices, and following up on that education with periodical reporting to all team members on the bank's financial performance and their contribution to the results. Armed with that knowledge, your employees will be far more likely to limit behaviors that benefit one group and not another, from reducing rate exceptions to ensuring that customers get placed in products that are truly best for them. Optimizing performance to all three major constituencies will ensure that your people will indeed do the right thing for both customers and shareholders |